Workers in Latin American and Caribbean (LAC) countries are paying around two-thirds less tax than those in OECD countries, according to a new report by the OECD Development Center, the OECD Center for Tax Policy and Administration, the Inter-American Center of Tax Administration (CIAT), and the Inter-American Development Bank (IDB).

The average worker in LAC countries paid an estimated 21.7% tax and social security contributions (SSCs) in 2013, compared to 35.9% in OECD nations. The estimation was calculated using the tax wedge, which considers the total taxes and compulsory SSCs paid by both employees and employers, after deducting any family benefits received.

Low Personal Income Tax

The main reason for this, according to the report, is that the vast majority of workers in LAC countries do not have to pay personal income tax (PIT) due to having incomes that are below the minimum PIT thresholds. In fact, of the 20 LAC countries assessed, it was only in Mexico that average workers were liable for PIT.

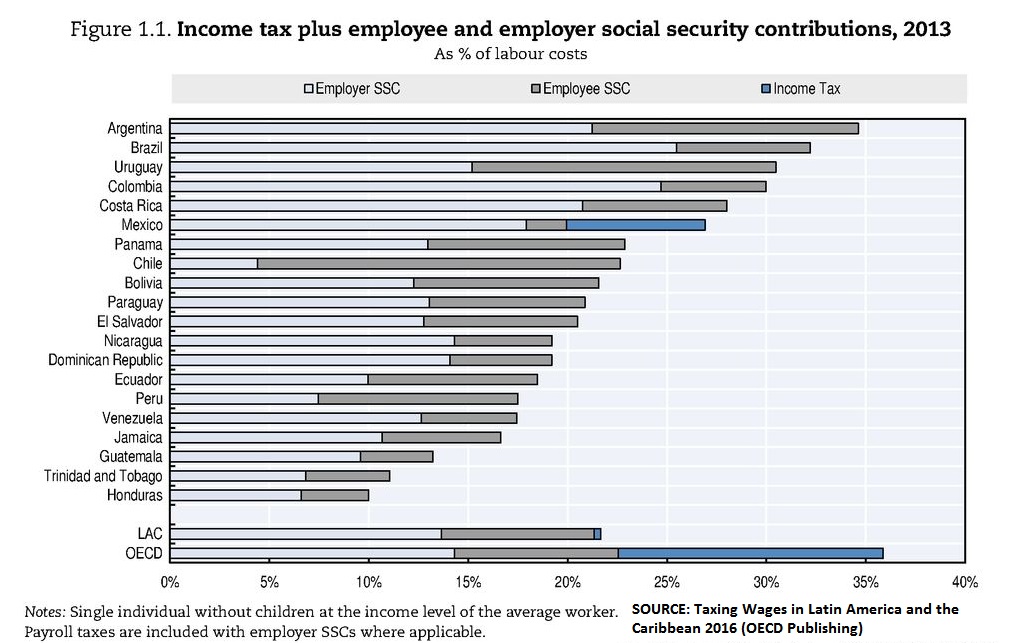

In LAC nations, the average tax wedge of 21.7% is made up of PIT (0.3%), employee SSCs (7.7%), and employer SSCs (13.6%). In comparison, the average of 35.9% in OECD nations is 13.3%, 8.3% and 14.3%, respectively.

Employees in LAC countries were found to have paid an average of 9.3% tax from their gross earnings in 2013. The majority of this cash (8.9%) was paid through employee SSCs, while the remaining 0.4% was for PIT. To compare again with OECD countries, the personal tax rate was 25.4% of gross earnings, 9.9% going to employee SSCs and 15.5% being PIT. “This highlights the difference in capacity of PIT to generate tax revenues from labor earnings in the OECD compared with LAC countries,” states the report.

Regional Differences

The LAC countries covered in the report are Argentina, Brazil, Bolivia, Chile, Colombia, Costa Rica, the Dominican Republic, Ecuador, El Salvador, Guatemala, Honduras, Jamaica, Mexico, Nicaragua, Panama, Paraguay, Peru, Trinidad and Tobago, Uruguay, and Venezuela, each of which has its own unique statistics.

Argentina is at the top of the tax wedge spectrum at 34.6%, while Honduras has the lowest at 10%. Brazil, Uruguay, and Colombia also have figures of 30% or more, while Guatemala and Trinidad and Tobago fall below the 15% mark.

Household Variations

The report is focused on taxes applied to the wage earnings of full-time employees in the formal sector, while considering personal circumstances (such as marriage and kids) to better estimate their position.

There are only small variations in the LAC tax wedge between workers with children and workers without. The average tax wedge for married couples with one breadwinner and two children was 21.4%, only 0.3 percentage points below the regional average. In OECD nations, where family allowance benefits were significantly more generous, the difference was a much higher 9.5 percentage points. Only 5 out of the 20 LAC countries had family allowance schemes, namely Brazil, Argentina, Colombia, Chile, and Uruguay.

Taking a broader look at the statistics, the average tax wedge for a worker without children ranged from 10.8% in the first income decile (people with the lowest 10% of earnings in the population) to 25.9% in the tenth income decile (the top 10% of earners). In comparison, the averages for married couples with two children and one earner were 7.1% and 25.7%, respectively.

The Informal Economy

While Latin American labor markets have been progressing rapidly over the last decade or so, increasing the levels of formal employment across the board, the informal economy (i.e. unrecorded cash transactions) is still very present, with countries like Honduras, Guatemala, and Nicaragua possibly having informality rates of over 80%.

These informality rates are generally higher in the first income quintile (lowest 20% of earners), according to the report. But, interestingly, countries such as Uruguay, Costa Rica, and Chile actually have the lowest informality rates in the same bracket, at 56%, 52%, and 41%, respectively. Even so, results also show that informality is still high among middle-income workers at 64%, and even hits 42% for workers in the fifth quintile.

High Employee Turnover

While the regional talent crisis continues to cause concern in the IT services industry, it seems that this crisis might extend to regional employment in general. “The region is trapped in a ‘vicious cycle’ of high employment turnover, low productivity, high labor costs, and high informality,” states the report. “High employment turnover discourages workers from seeking more on-job education and training, which could otherwise result in employment relationships that generate increases in productivity”

Linking this issue to the average tax figures in LAC countries, it is clear that low labor productivity relative to the costs (taxes, SSCs) of formality is acting as a petri dish for the informal market. Furthermore, many workers in LAC countries lack any form of unemployment insurance, meaning they cannot afford the time to find a job more suited to their skills, and end up taking anything they can find in order to pay the bills.

Ultimately, Latin American and Caribbean nations still have a ways to go to break this ‘Catch-22’ situation that many workers find themselves in, and perhaps the situation calls for new taxation policies and social insurance programs to ensure the right environment for the creation of quality jobs.

You may also like

Add comment