Latin America as a hub of business and IT service delivery has grown fast in recent years. This growth includes the presence of major third-party services providers and smaller outfits alike, shared service centers, and IT outsourcing firms of all sizes. And it encompasses every sub-region of Latin America. Beneath the headline though, the industry is itself being remade due to technological change, ranging from the automation of services to the provision of Software-as-a-service (SaaS). However, the full implications of this shift may not be realized for years. (A summary powerpoint of the State of Nearshore 2016 report is found here.)

At such junctures, it’s often a good idea to take stock, both in order to gauge performance and to ponder how nearshore can cope with the challenges ahead. With this in mind, Nearshore Americas conducted a survey in March and April of 2016, in which 144 outsourcing professionals registered their views on the benefits of nearshore delivery, the characteristics of particular geographies, and the outlook for the region amid rapid technological change in the business services industry.

Breaking Down Nearshore into Key Components

One survey goal was to break down nearshore as a value proposition by identifying how the key components of nearshore delivery—arbitrage, time-zone alignment, proximity, business culture affinity—positions markets differently. As one might expect, the survey respondents considered cost as the most important factor in the decision on where to locate service operations. This continues to cause angst among many service providers because they sense business is being lost to lower cost locales like India.

Negotiating Headwinds

Several Latin American currencies have experienced historic depreciation since 2014. Outsourcing contracts are increasing in number but not in net value. Re-shoring is gaining steam. Digital disruption seemingly threatens the business model of many firms. Suffice to say, nearshore vendors have encountered their share of challenges lately.

Yet, the survey respondents registered optimism that the industry overall will successfully negotiate these challenges in the near term. Over 40% of respondents said that currency volatility amounts to a competitive advantage for vendors, far eclipsing the 10% who said that companies are likely to leave the region as a result of the volatility. And over half of the survey respondents noted that digital disruptions either will not affect their willingness to invest in nearshore delivery or else it will make them more likely to invest in nearshore operations.

When it comes to re-shoring though, respondents were more guarded. When asked if re-shoring was a threat to nearshore 30% said no, 19% said yes and 51% said it remains to be seen.

Cautious Optimism about the Future

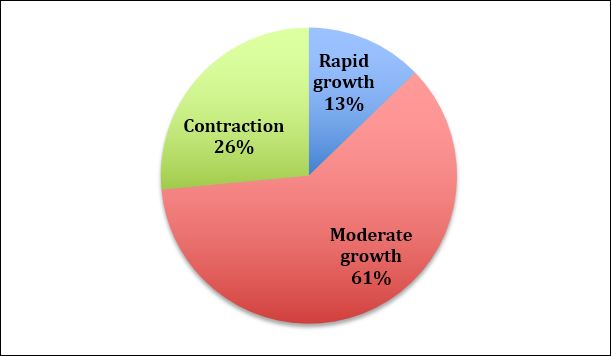

Looking ahead, survey respondents registered cautious optimism about nearshore delivery. Once-hot markets like Costa Rica are slowing, due in part to rising wages. While the baseline forecast for Costa Rica is moderate growth through 2019, twice as many nearshore survey respondents said they expect the BPO/ITO industry to contract as those who said the market was poised for rapid growth in the years ahead.

However, the biggest drag on nearshore growth may be perceptions of physical security. Negative perceptions of Latin America registered as the biggest challenge to nearshore viability by a 25-point margin over the second most often cited concern, rising wages. Nowhere is the problem of perception vs. reality greater than in Mexico. In fact, respondent perceptions of markets that are considered safe dovetails with the World Bank’s calculation of the homicide rate for Argentina, Brazil, Colombia and Peru. Mexico is the only market where the perception of the country as “unsafe” is significantly above the actual homicide rate.

While Mexico grapples with misperceptions, the global services industry is expanding to include emerging geographies. Given that technology is fast taking over the workload once performed by humans with a lower educational skill set, late entrants will do well to match workforce strengths with in-demand niches. Key among these emerging geographies is the Caribbean. The main focus of delivery is call centers, though, as the survey highlighted, large Caribbean islands like Jamaica are also well positioned to deliver higher value IT and knowledge services.

Overall, the nearshore appears to be transitioning from a rapid growth trajectory to a more moderate one. This may disappoint those hoping for double-digit growth across the region, but it is in line with industry trends in other regions. More importantly, it is a sign that the nearshore is maturing as an industry.

For more insights, and to download the State of the Nearshore 2016 report for free, visit here.

You may also like

Add comment